Values-Based Budgeting: Align Spending With What You Actually Care About

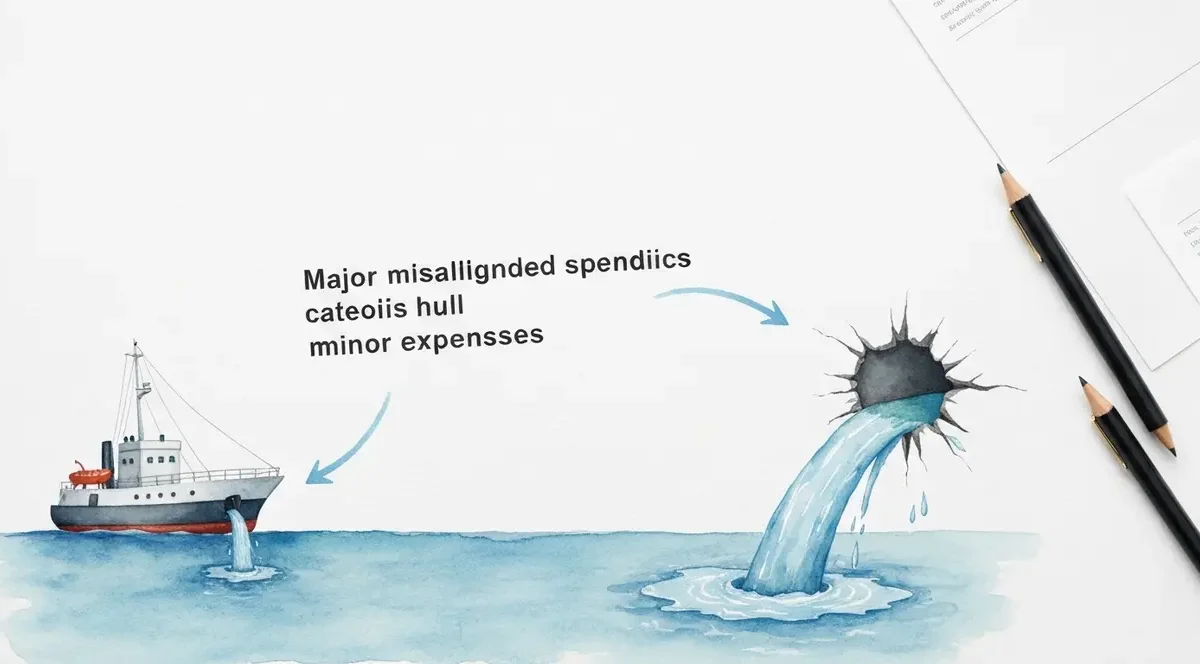

The leaks that sink budgets are not the small ones. They are big spends on things you do not even care about.

“Beware of little expenses; a small leak will sink a great ship,” Benjamin Franklin wrote in The Way to Wealth back in 1758. He was right about the leak, but he missed half the story: the leaks that actually sink modern households aren’t the small ones. They’re the big ones flowing into categories the household doesn’t even care about. That’s why values-based budgeting beats traditional cutting on almost every measure that matters.

Here’s the gap nobody talks about. A 2025 Empower survey found 44% of Americans call the memories they make while traveling “priceless,” yet roughly 1 in 3 planned to spend less on travel that same year. Meanwhile, dining out, streaming, and convenience purchases kept rolling on autopilot. Stated priority on one side, actual spending on the other, and almost nobody reconciles the two. That reconciliation is the whole game.

The one rule, and when it breaks

The rule is simple: every recurring dollar should map to something you’d defend out loud if a friend asked why you spent it. If you can’t defend it, you’re not spending well, no matter how cheap the item was. This single test outperforms most budgeting apps because it doesn’t care about categories. It cares about intent.

That said, the rule has real exceptions. Don’t apply it to the following:

• Fixed essentials. Rent, utilities, insurance, minimum debt payments. These aren’t priority decisions; they’re floor decisions.

• Emergency fund contributions. Savings isn’t a “value” in the emotional sense, it’s the structure that protects every other value.

• Tax-advantaged retirement matches. A 401(k) match is free money, full stop. Don’t philosophize about whether retirement “aligns with your values” while leaving the employer match on the table.

• Health and preventive care. The dentist visit you keep postponing isn’t a values question.

Everything else is fair game for the alignment test. And “everything else” is usually 40-60% of household outflows, which is exactly where the real money lives.

I’ve seen people apply the rule to their mortgage and torture themselves over a fixed cost they can’t change for two years. Don’t do that. Apply it where you have leverage: subscriptions, dining, retail, transportation choices, gifts, hobbies, the small recurring items that compound into thousands a year.

The exercise: top 3 priorities vs. top 3 spending categories

Grab a pen, let’s do the math together. Take a blank sheet. On the left, write your three top life priorities. Not aspirational ones, the real ones. Family time. Travel. Fitness. Learning a new skill. Building a business. Owning a home. Whatever it actually is when you’re honest. On the right, pull up your last 90 days of bank and credit card statements and list your three biggest discretionary spending categories by dollar amount. Not by transaction count, by total dollars.

Now compare. In the thousands of statements I reviewed back at the bank, the match rate between stated priorities and top three discretionary categories was somewhere around 1 in 5. Four out of five people had a clear mismatch, and most of them had no idea until they saw the two columns side by side. A client once told me her priority was “saving for a down payment.” Her top three discretionary categories were food delivery, a clothing subscription she’d forgotten she had, and rideshare to a gym she went to twice a month. None of those were wrong on their own. They were wrong relative to what she said she cared about.

The reconciliation step is where it gets practical. For each mismatched category, you have three options: cut it (if it’s pure default spending), reduce it (if it’s somewhat enjoyable but not priority-aligned), or reframe it (if you can change how you spend within the category to better serve a priority). The clothing subscription got cut. The food delivery got reduced to twice a week. The rideshare got reframed into a closer gym she could walk to. Net result: roughly $380 a month redirected to the down payment fund, without feeling deprived for a single day.

Why this beats “just cut more”

Traditional budgeting tells you to spend less. Values-based budgeting tells you to spend differently. The difference matters because deprivation budgets fail. They fail predictably, usually within 60 to 90 days, because they’re built on willpower. Alignment budgets succeed because they’re built on preference. You’re not fighting yourself; you’re funding the version of your life you already said you wanted.

The data backs this up. A January 2026 KeyBank Pulse Poll found 88% of Americans had made at least one meaningful financial adjustment, with switching to cheaper brands as the most common move (59%, up from 49% the year before). That’s reactive cutting. It works for a quarter and then quietly reverses when the budget pressure eases. Compare that to readers who tell me they restructured their spending around two or three core priorities two years ago and never looked back. The behavior sticks because the motivation isn’t external pressure, it’s internal alignment.

There’s also a saving rate angle. The U.S. personal saving rate has been hovering around 3.5% in late 2025, which is historically low. Most people assume they can’t save more because they don’t earn enough. In my experience reading household cash flows, that’s true maybe 30% of the time. The other 70%, there’s room. It’s just buried under default spending in categories the household doesn’t actually care about. Values-based budgeting surfaces that room without asking anyone to earn another dollar.

Smarter approaches that actually stick

Once you’ve done the reconciliation, the maintenance work is lighter than people expect. A few approaches that compound over time:

• Quarterly check-ins. Every three months, re-rank your top three priorities and re-pull your top three spending categories. Life shifts. So should the budget.

• Subscription audit. Pull your statement and circle every recurring charge. For each one, ask: would I sign up today if I weren’t already paying? If not, cancel this week.

• One-in, one-out rule. Adding a new recurring expense requires removing one. Forces priority thinking at the moment of decision.

• Priority-funded sinking funds. If travel is a top three priority, open a separate high-yield savings account labeled “Travel” and automate a monthly transfer. The dedicated bucket protects the priority from getting raided for default spending.

Notice none of this requires a complicated spreadsheet or an app subscription. Frequency beats complexity, every time.

The other approach that works better than people think is automating the alignment. If your top priority is retirement, max the 401(k) match through payroll deduction before the money ever hits checking. If it’s emergency savings, set the auto-transfer for the day after payday, not the day before the next one. Money you never see in checking is money you never default-spend.

The plan that beats the spreadsheet

Franklin’s leak metaphor was almost right, just pointed at the wrong leak. The little expenses aren’t sinking the ship; the medium-sized ones flowing into categories you don’t even rank in your top three are. The fix isn’t a smaller boat, it’s pointing the hose at the right deck. Once you see your spending and your priorities in two columns, the gap practically closes itself.

Three reader profiles, three different plays:

• Tight budget, under $50k household income: skip the elaborate exercise. Pick your single highest priority, automate one transfer to fund it, and cancel two subscriptions this week. That’s the whole plan for now.

• Middle income, $50k-$120k, some slack in the budget: do the full top-three exercise this weekend. Expect one to two genuine surprises. Redirect $200-$500 a month from mismatched categories to priority-funded sinking funds.

• Higher income, $120k+, complex spending: the alignment work matters more, not less. Higher incomes hide more default spending. Run the exercise quarterly, not annually, and pay attention to lifestyle creep on the categories you don’t actually value.

Here’s what usually goes wrong when readers try this. First, the priority list gets contaminated by what they think they should care about instead of what they actually do. If you write “fitness” because it sounds responsible but you haven’t worked out in eight months, the whole exercise breaks. Be honest. Second, the spending review pulls one month instead of three, which hides quarterly subscriptions and seasonal patterns. Pull 90 days minimum. Third, people try to cut everything mismatched at once, which feels punitive and reverses inside a month. Pick the top two mismatches, fix those, leave the rest alone for the next quarter.

Back at the bank, I had a manager who reviewed her own statement every Sunday morning for ten minutes. Coffee, statement, pen. That was her entire system, and her household saving rate was triple the branch average. The lesson stuck with me: alignment isn’t a spreadsheet, it’s a habit. The spreadsheet is just where you write down what the habit already decided.

This weekend, do this exact thing. Pull 90 days of statements from your primary checking and your most-used credit card. Write your top three real priorities on one side of a page and your top three discretionary spending categories on the other. Circle every mismatch. Pick the two biggest, decide cut, reduce, or reframe for each, and set up one automated transfer to fund whichever priority is currently underfunded. For deeper reading on the framework, the Consumer Financial Protection Bureau has solid free planning tools, and Bureau of Labor Statistics consumer expenditure data is useful for benchmarking your categories against national averages.